What is mortgage stress? Understanding, identifying, and overcoming it

Everyone wants to protect their home, so what is mortgage stress in your home loan and how do you overcome it? Mortgage stress occurs when a household spends a significant portion of its income, often defined as over 30% of pre-tax earnings, on mortgage repayments, leaving little room for other essential expenses. This financial strain is exacerbated by rising living costs, interest rate hikes, or unexpected life events such as job loss or medical emergencies.

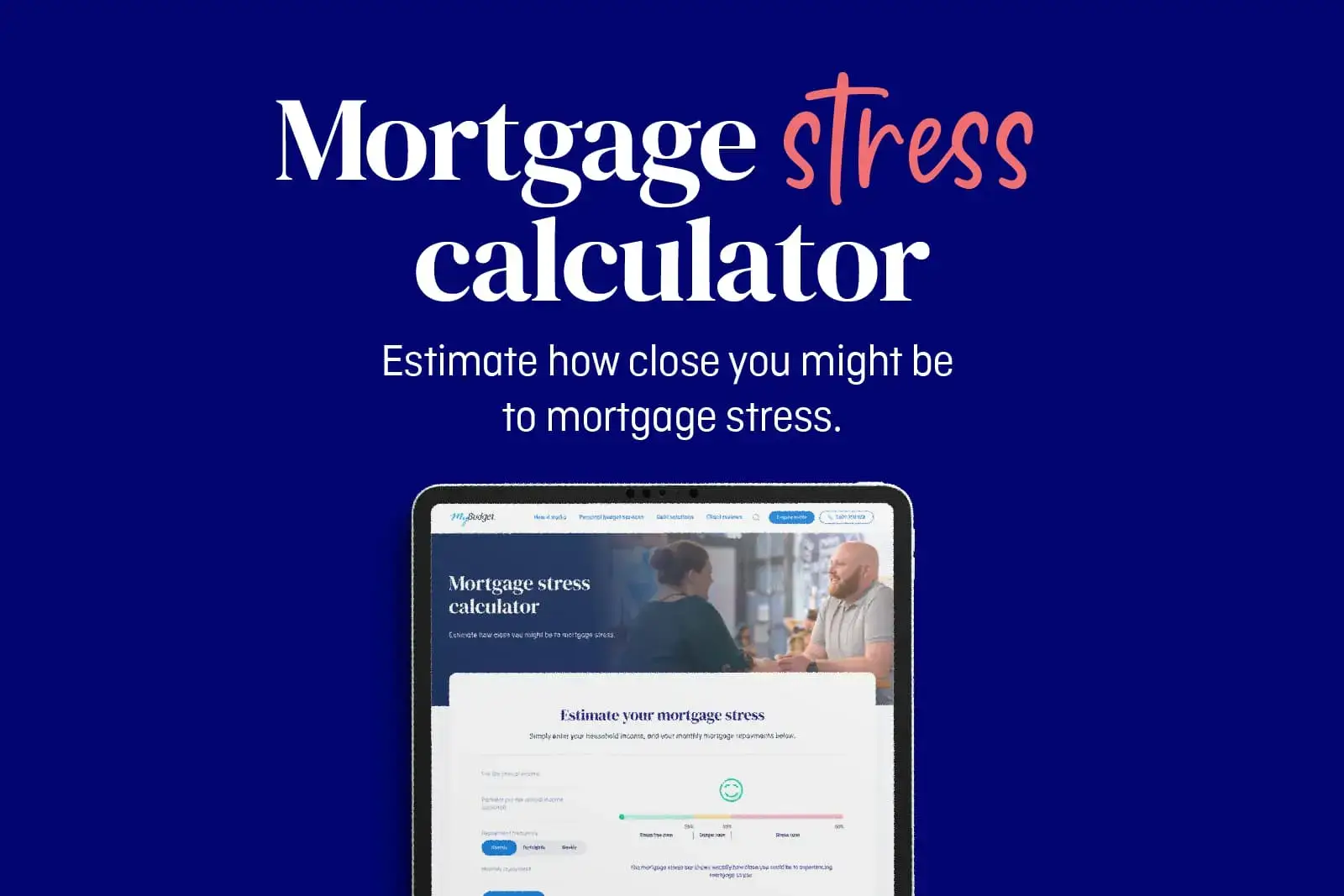

In Australia, mortgage stress is a growing concern, with 26.8% and growing of mortgage holders reportedly at risk. But how can you determine if you’re affected? That’s where tools like MyBudget’s Mortgage Stress Calculator come in handy.

We’re seeing pressure right across Australia, but it’s particularly tough in areas with higher property prices and larger loan sizes.

Tammy Barton | MyBudget, Founder & Director

Signs of mortgage stress

Difficulty meeting repayments

Struggling to pay on time or dipping into savings.

Cutting back on essentials

Reducing spending on groceries, utilities, or healthcare to prioritise mortgage payments.

Increased debt dependence

Relying on credit cards or personal loans to cover expenses.

Emotional and physical stress

Anxiety, sleeplessness, and strained relationships.

What causes mortgage stress?

Mortgage stress can arise from various factors:

Interest rate hikes

Higher rates lead to larger monthly repayments.

Loss of income

Job loss or reduced hours can significantly impact financial stability.

Unexpected expenses

Medical emergencies or urgent home repairs can disrupt budgets.

Over borrowing

Taking on a mortgage that stretches finances too thin.

“Long-term, it can damage your credit score, limit future borrowing options, and delay achieving your financial goals.”

Tammy Barton, MyBudget Founder & Director

How to determine if you’re in mortgage stress

The free MyBudget Mortgage Stress Calculator simplifies this process:

- Enter your household income and monthly mortgage repayments

- Select your repayment frequency

- View your result:

- Stress-Free Zone: Repayments < 20% of pre-tax income

- Danger Zone: Repayments between 20%-30%

- Stress Zone: Repayments > 30%.

This visual tool helps you understand where you stand and offers actionable insights.

How personal budgeting can help

At MyBudget, we specialise in creating tailored budgets to help you regain financial control. Here’s how we support you:

- Plan ahead: your income and expenses are mapped out 12 months in advance.

- Automate finances: we manage your bills, savings, and repayments.

- Build emergency savings: every budget includes a safety net for unexpected expenses.

- Tailor to your lifestyle: enjoy date nights, holidays, or savings for a house deposit, all part of your personalised plan.

- Dedicated support: “I can call MyBudget feeling completely stressed out about an unexpected bill or circumstance, and I always finish off the call feeling relieved and confident that my money is in good hands.” – Sarah, current MyBudget client

Practical steps to manage mortgage stress

- Review your budget: use MyBudget’s tools and expertise to identify savings opportunities

- Talk to your lender: they may offer options like temporary repayment reductions or refinancing

- Explore additional income streams: consider part-time work or renting out a spare room

- Seek professional help: MyBudget provides personalised financial guidance tailored to your situation.

Why choose MyBudget?

Financial stability isn’t just about managing numbers, it’s about peace of mind. With MyBudget’s Mortgage Stress Calculator and expert support, you can:

- Reduce financial strain

- Gain clarity on your finances

- Achieve long-term financial goals.

Take action today

Don’t let mortgage stress take over your life. Use the Mortgage Stress Calculator to assess your situation, and let MyBudget help you build a brighter financial future.

Ready to transform your finances? Start your personal budgeting journey with MyBudget today.

This article has been prepared for information purposes only, and does not constitute personal financial advice. The information has been prepared without taking into account your personal objectives, financial situation or needs. Before acting on any information in this article you should consider the appropriateness of the information having regard to your objectives, financial situation and needs.