What are the 25 Best side hustles in 2026

19 min read

In Australia, most lenders require a 5-20% deposit to buy a home. A 20% deposit avoids lenders mortgage insurance (LMI), while a 5-10% deposit may be possible through schemes like the First Home Guarantee, depending on eligibility and lender requirements.

Saving for a house deposit in Australia can feel like an impossible dream, especially with property prices rising like they have been over the past few years. However, with the right budget plan and consistent savings strategy, many buyers reach their goal sooner than they expect. Creating a clear personal budget is often the first step towards building a deposit faster. Whether you’re a first-time buyer or returning to the market, this guide will show you how to save for a house deposit and secure your dream home.

Property prices in Australia have been climbing for decades, making it increasingly difficult for first-home buyers to save a deposit and enter the market. According to Cotality’s Home Value Index (March 2026), Australian dwelling values have continued rising over the past year, increasing the savings target buyers need to reach before purchasing a home. Many lenders require a 20% deposit saved up to avoid paying Lenders Mortgage Insurance (LMI). For a $750,000 home, that’s $150,000, a significant sum to save, particularly while managing rent and other expenses.

One of the most common questions people ask is how much is a deposit for a house? The answer depends on the property price your targeting, the lender, and whether you’re aiming to avoid Lenders Mortgage Insurance (LMI). As a rule of thumb, a 20% deposit is often seen as the benchmark because LMI is usually charged when you borrow more than 80% of the property value. Lenders assess this using the Loan to Value Ratio (LVR), which compares the size of your loan to the value of the property. Some buyers enter the market with a 5% or 10% deposit, especially if they’re using government support schemes or are comfortable with higher upfront and ongoing loan costs. In other words, the “right” deposit is not just about getting approved, it’s about what leaves you with manageable repayments once you own the home.

Property Price | 5% Deposit | 10% Deposit | 20% Deposit |

$650,000 | $32,500 | $65,000 | $130,000 |

$750,000 | $37,500 | $75,000 | $150,000 |

$900,000 | $45,000 | $90,000 | $180,000 |

$1,000,000 | $50,000 | $100,000 | $200,000 |

$1,250,000 | $62,500 | $125,000 | $250,000 |

$1,500,000 | $75,000 | $150,000 | $300,000 |

$1,750,000 | $87,500 | $175,000 | $350,000 |

$2,000,000 | $100,000 | $200,000 | $400,000 |

Lenders Mortgage Insurance (LMI) is a fee charged when a borrower purchases a property with less than a 20% deposit. The insurance protects the lender, not the borrower, and can add thousands of dollars to the cost of buying a home.

Yes. Several Australian government programs allow eligible buyers to purchase with smaller deposits:

A smaller deposit may help you buy sooner, but it usually means borrowing more, paying more interest over time, and potentially paying LMI, unless you qualify for an eligible scheme.

The time it takes to save for a house deposit depends on your income, expenses and the property price you’re targeting. For many Australians, saving a 20% deposit can take several years, but with focused budgeting and lifestyle changes it can happen much faster.

To illustrate how achievable saving for a house deposit actually can be, let’s consider the hypothetical story of Tom and Olivia. This couple, with a combined income of $170,000 per year before tax and $11,163 per month after tax, represents many Australians who find it challenging to save for their first home deposit due to their lifestyle choices. By making specific changes, they can manage to save $150,000 for a house deposit in just 18 months. Here’s a closer look at their story:

Tom is a 31-year-old high school teacher earning $90,000 per year before tax, which translates to approximately $5,866 per month after tax. Olivia, 30, works as a dental nurse earning $80,000 annually, or about $5,297 per month after tax. They live in a rental apartment in Melbourne’s suburbs, paying $4,000 per month. Both are outgoing individuals who love socialising, dining out, travelling, and enjoying hobbies like gym workouts and barista-made coffee. Tom is a car enthusiast who owns two vehicles, while Olivia enjoys spa treatments and weekend movie outings. Without knowing it, they’ve inadvertently chosen their lifestyle above saving for a home, which is still possible if they make some changes.

Despite their good incomes, Tom and Olivia found themselves living paycheck to paycheck, with little to no savings. Realising that they needed to make significant lifestyle changes to achieve their goal savings up for a deposit and then enjoying homeownership, they set out on a structured journey to save. The first step was creating a clear plan for where their money would go each month and how they could consistently build their deposit.

Personal budgeting was their first step. They calculated that to save $150,000 in 18 months, they would need to set aside $8,350 monthly. This daunting figure motivated them to take a hard look at their finances to work out how they can create a savings plan for their deposit. Together, they tracked every expense, including rent, utilities, and discretionary spending, to identify areas where they could make cuts.

Key Tip: use the free MyBudget Personal Budget Template or ask about the MyBudget app to gain clear insights into your spending patterns.

With a clear understanding of their expenses, Tom and Olivia identified specific areas for savings to help put money aside to save for their home:

They moved to a smaller, more affordable rental in a different suburb, saving $1,000 per month to go toward their monthly goals. Subletting a spare room added $1,600 per month to their income which they instantly put into their house deposit savings account.

Tom’s decision to sell his second car not only provided an immediate $4,000 cash boost but also reduced ongoing costs like insurance, registration, and maintenance.

Dining out was reduced by half, saving $15,000 over 18 months. They postponed holiday plans, saving an additional $10,000.

For Tom and Olivia, savings became satisfying. Transferring money every month into a joint high interest rewarding savings account was exciting, and with extra interest they could visualise their journey toward saving for a house deposit and home ownership.

Here’s how Tom and Olivia saved $8,350 per month to build up their $150,000 house deposit in 18 months:

Total monthly expenses after changes: $2,813.

Savings after expenses: $8,350 per month. Did we mention Tom is a maths teacher?

The sale of Tom’s second car for $4,000 gave them a financial boost early on, further motivating their savings journey.

Every dollar they saved toward their house deposit went into a high-interest savings account. They actually opened a rewards saver account so their savings could benefit from compound interest over time. Having a high interest savings account helps keep you motivated and focused on your house deposit savings goal.

Key Tip: Automatic transfers eliminate the temptation of spending.

It’s also smart to look beyond the deposit itself and think about what comes next. Repayments, rates and your borrowing power all affect how much home you can comfortably afford. A lot of buyers focus on reaching a deposit target that they forget to test whether the future mortgage will still be comfortable if interest rates rise, bills increase, or one income temporarily drops. That’s where the MyBudget Home Loan Repayment Calculator becomes useful. It can help buyers estimate repayments across different loan amounts, terms and interest rates, so they can see the real difference between buying with a 5%, 10% or 20% deposit and understand what that means for their monthly budget.

Deposit size | What it usually means |

5% deposit | Lower upfront savings target, but larger loan amount, higher repayments, and often LMI unless eligible for a government scheme |

10% deposit | More achievable than 20% for some buyers, but still likely to mean higher repayments and possible LMI |

20% deposit | Higher savings target upfront, but lower loan amount, lower repayments, and often no LMI |

While the initial lifestyle changes were challenging, Tom and Olivia adapted quickly. They found joy in cooking meals at home, exploring free local activities, and watching their savings grow. By the end of 18 months, they had reached their goal of $150,000 (20% of $750,000) and were ready to purchase their dream home.

But does this savings plan for a new home deposit work in the real world?

Deposits vary widely depending on where you’re buying and which lender you’re borrowing from. While every suburb and property type is different, looking at median dwelling values can help you estimate what a realistic savings goal looks like. For example, a 20% deposit in Sydney is different to a 20% deposit in Darwin, which is why people benefit from setting a location based savings target rather than chasing a generic deposit figure.

City | Example dwelling value | 5% deposit | 10% deposit | 20% deposit |

Sydney | $1,300,000 | $60,000 | $130,000 | $260,000 |

Brisbane | $1,080,000 | $50,000 | $110,000 | $220,000 |

Perth | $990,000 | $50,000 | $100,000 | $200,000 |

Adelaide | $920,000 | $50,000 | $90,000 | $180,000 |

Canberra | $900,000 | $50,000 | $90,000 | $180,000 |

Melbourne | $830,000 | $40,000 | $80,000 | $170,000 |

Hobart | $730,000 | $40,000 | $70,000 | $150,000 |

Darwin | $600,000 | $30,000 | $60,000 | $120,000 |

These figures show why people asking “how much deposit for a house” has no one-size-fits-all answer. A buyer in Canberra may be targeting a deposit that is less than half the size of what a buyer in Sydney may need for a comparable 20% strategy. That’s also why breaking your deposit goal into smaller monthly milestones matters so much. Once you know your likely purchase price range, you can work backwards and build a savings plan that feels specific, measurable and achievable. Median dwelling values shown above are based on Cotality’s Home Value Index results for February 2026.

Like many of us, Erin and Adam initially tackled their personal budgets and finances with spreadsheets. “We had a spreadsheet we checked three or four times a day,” Erin shared. “We were so scared of dipping into our savings for our apartment deposit that we tracked every dollar obsessively.”

But after working with MyBudget, Erin realised their spreadsheet had gaps, expenses they hadn’t accounted for, like Christmas or emergency service levies. “It became obvious we were missing so much,” Erin said. “Our spreadsheet didn’t prepare us for things that seemed predictable but always caught us off guard. MyBudget highlighted all those blind spots for us.” They needed a savings plan.

Erin was the first to embrace the idea of outsourcing their budget especially as saving for a home deposit was one of their real world goals. “I was sold from the start,” she said. “Adam was hesitant, but once we saw what MyBudget could offer, it was a no-brainer.”

One of the biggest revelations MyBudget’s technology highlighted to the couple? The gaps in their financial budgeting. “We never set aside money for Christmas, how wild is that?” Erin laughed. “Every year, we’d dip into savings or rack up credit card debt for presents, and every January would feel like a financial hangover.”

MyBudget’s tailored budgeting service helped Erin and Adam account for annual expenses like Christmas, car registration, and emergency service levies, ensuring their financial goals stayed on track. “It gave us a full picture of where our money was going and how to plan for the future,” Adam said, “and budget for and help us reach our savings goals.”

With a Personal Budgeting Plan from MyBudget, in just two years, Erin and Adam saved over $70,000 for a deposit on their dream home, thanks to their commitment to sticking to the plan and rethinking their spending habits. They made simple swaps, like replacing their daily café coffees with homemade brews, saving $4,000 in a year. They also planned a $5,000 family holiday to Fiji in just six months, all while Erin was on maternity leave. – With twins, no less!

Grocery shopping became another success story. Before MyBudget, their food bills were unplanned and often exceeded expectations. Now, Erin carefully plans weekly food shops for their family of four under $225. “This just wouldn’t be possible without MyBudget,” Erin said who uses the free MyBudget Healthy meal planning on a budget guide to save money on food without compromising on nutrition.

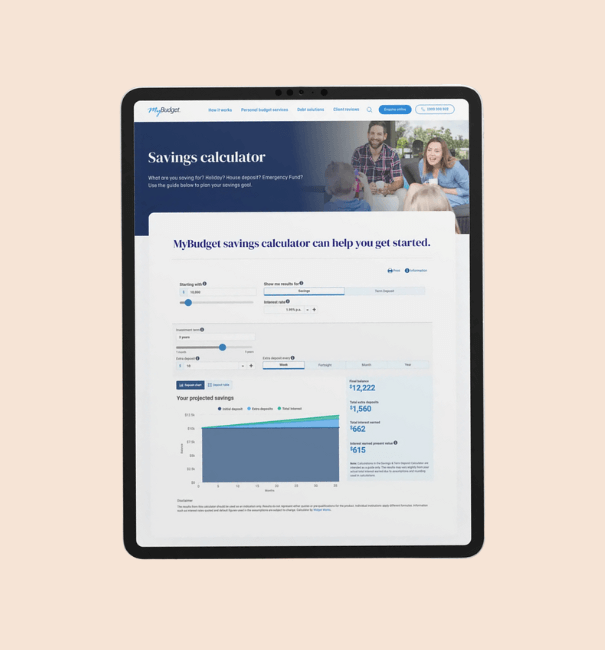

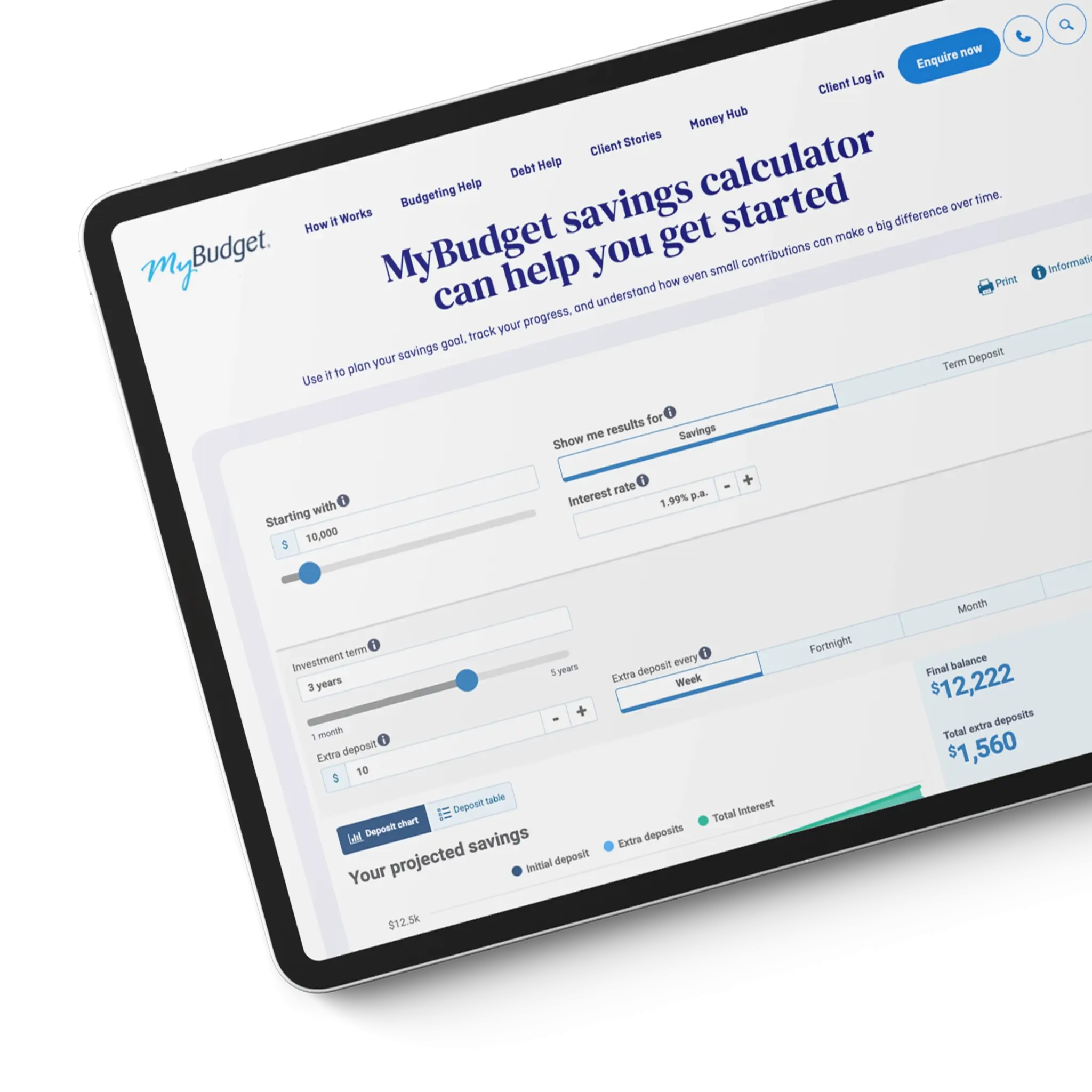

Want to see how much you could save by making small changes? Check out MyBudget’s free Savings Calculator. Seeing how you can save for that home deposit quicky, and visualise how can be exciting.

A house deposit is only part of the total home buying costs you’ll need to save before purchasing a property. Buyers should also budget for upfront costs such as stamp duty, conveyancing or solicitor fees, inspections, loan application fees and moving costs. Creating a clear budgeting plan can help buyers see the full picture of these costs before they commit to purchasing a home. If you focus only on the deposit and ignore purchase costs, you may reach your savings target and still find yourself short when it’s time to buy. This is another reason people benefit from a full budgeting plan rather than a simple spreadsheet. Your savings goal should reflect the true cost of getting into a home, not just the headline deposit figure.

Example home price | 10% Deposit | Estimated LMI fees | Example inspection / legal fees |

$1,000,000 | $100,000 | $25,000 | $2,500 |

On a $1,000,000 home, a buyer aiming for a 10% deposit may need to save around $130,000, not just the $100,000 deposit. That estimate includes an additional $25,000 in Lenders Mortgage Insurance (LMI) plus around $2,500 for building and conveyancing or legal costs. The exact amount can vary depending on your lender, loan structure and location, but this example shows why buyers should budget for more than the deposit alone. It also does not include stamp duty or transfer fees, which can add more depending on the state or territory. LMI is generally charged when you borrow more than 80% of the property value, while typical inspection and conveyancing costs commonly run into the low thousands.

Download MyBudget’s Home Buyers Guide for tips on saving for your deposit, understanding the real upfront costs, and planning for the repayments that come after purchase. It’s a simple way to feel more confident before you take the next step toward buying your home.

Saving for a house deposit while renting can feel like trying to move forward while carrying extra weight, because rent is often the biggest expense in your budget. The key is to treat your deposit savings like a fixed bill, not something you only contribute to if there is money left at the end of the month. That may mean choosing a less expensive rental, sharing with a housemate, negotiating bills with your partner, cutting non-essential spending, and creating a dedicated savings account that your deposit money goes into automatically on payday.

Budget change | Example monthly impact |

Move to a cheaper rental | $300 to $800 saved |

Share accommodation or sublet a room | $500 to $1,500 saved |

Cut takeaway and dining out | $200 to $500 saved |

Cancel or reduce subscriptions and memberships | $50 to $150 saved |

Review groceries and meal plan | $100 to $300 saved |

Set up automatic weekly savings transfers | Builds consistency |

If your goal is to save for a house deposit in a year, the most important step is working backwards from your target. Once you know roughly how much you need, divide that figure into monthly, weekly and even daily amounts so the goal feels measurable. For example, saving a $60,000 deposit in 12 months means finding about $5,000 per month, while a $100,000 deposit means saving around $8,333 per month.

Deposit target | Monthly savings needed | Weekly savings needed |

$40,000 | $3,333 | $769 |

$60,000 | $5,000 | $1,154 |

$80,000 | $6,667 | $1,538 |

$100,000 | $8,333 | $1,923 |

$120,000 | $10,000 | $2,308 |

Reducing rent, boosting income, selling unused assets, pausing holidays, and temporarily trimming lifestyle expenses can all help make an aggressive savings goal more realistic.

Saving for a house deposit in Australia becomes far easier when you have a clear plan, a structured budget, and someone helping you stay on track. That’s exactly what MyBudget does.

For over 25 yearsMyBudget has helped more than 130,000 Australians organise their money, reduce debt, and build savings for major goals like buying a home. Instead of juggling spreadsheets or hoping there’s money left at the end of the month, our expert team helps you create a personalised budget that covers your bills, prioritises your savings goals, and helps you get back on track.

If saving for a house deposit feels overwhelming, you don’t have to do it alone.

See how MyBudget can help you create a clear plan to reach your home ownership goals sooner, or call us on 1300 300 922.

Can’t find what you’re looking for? See more FAQs…

Most Australian lenders prefer a 20% house deposit because it helps buyers avoid Lenders Mortgage Insurance (LMI). However, many first-home buyers purchase property with deposits as low as 5% or 10% using government programs such as the First Home Guarantee or through a guarantor home loan.

Yes. Eligible first-home buyers in Australia can buy a property with a 5% deposit through government initiatives like the First Home Guarantee. This scheme allows buyers to avoid paying Lenders Mortgage Insurance, making it easier to enter the property market sooner.

Yes. Many Australians successfully save for a house deposit while renting by treating savings like a fixed bill, reducing housing or lifestyle costs, and using automatic transfers to a dedicated savings account. Budgeting consistently and tracking spending can help renters build a deposit faster.

This article has been prepared for information purposes only, and does not constitute personal financial advice. The information has been prepared without taking into account your personal objectives, financial situation or needs. Before acting on any information in this article you should consider the appropriateness of the information having regard to your objectives, financial situation and needs.