Back

How much emergency fund should you have? And how to build it

Life is unpredictable, and emergencies can happen at any time. If you have ever felt like you are one unexpected expense away from things getting tight, that feeling is more common than you might think. A financial buffer gives you emergency money to fall back on, so you are not relying on credit cards, Buy Now Pay Later, or loans when something goes wrong.

Think of it as a financial safety net, a savings buffer in a separate savings account, ready for unexpected expenses when they arise. It is money set aside for real emergencies, not everyday spending, helping you stay in control and reduce financial stress.

In this guide, you will learn what an emergency fund is, how much you may need, how to start calculating your emergency fund, where to keep it, and simple ways to build it over time.

What is an emergency fund?

An emergency fund is money set aside to cover unexpected but necessary expenses, such as medical bills, urgent repairs, or a temporary loss of income. It acts as a financial safety net so you do not need to rely on debt like BNPL, or early wage access when something goes wrong.

It is there to help cover costs you cannot always plan for, such as:

- Medical bills

- Urgent car repairs

- Essential home repairs

- Temporary loss of income

- Unexpected travel for a family emergency.

Without emergency money set aside, many people rely on debt to cover surprise costs, which can add financial pressure through interest and repayments, especially if high-interest debt is involved.

Why is an emergency fund important?

An emergency fund helps reduce financial stress, avoid debt, and keep you on track when unexpected costs arise. Without one, it is easy to feel like you are constantly reacting instead of being in control. It gives you breathing room so one setback does not derail your entire budget or monthly expenses.

Even a short disruption to income can impact rent or mortgage repayments, groceries, utilities, transport, and insurance. Having a buffer helps you stay in control, rather than scrambling to cover costs.

How much emergency fund should you have?

At MyBudget, we recommend aiming for 3 months of essential living expenses in an emergency fund. If you have been unsure what the ‘right’ number is, this gives you a clear place to start. This provides a buffer if income stops or a major unexpected expense occurs.

The exact amount depends on your situation:

- Stable income: around 3 months of essentials

- Variable income or self-employed: 3 to 6 months

- Starting out: even $500 to $1,000 is a strong first step.

How much should your emergency fund be based on your expenses?

Your emergency fund should be based on your essential monthly expenses and how many months you want to cover. The table below shows how your target changes depending on your spending and savings goal.

Monthly essential expenses | 1 month buffer | 3 month buffer | 6 month buffer |

$2,000 | $2,000 | $6,000 | $12,000 |

$3,000 | $3,000 | $9,000 | $18,000 |

$4,000 | $4,000 | $12,000 | $24,000 |

$5,000 | $5,000 | $15,000 | $30,000 |

If three months feels out of reach, start smaller. A $1,000 emergency fund is still protection.

Not sure what your monthly expenses are? Try our free Personal Budget Template to get a clear picture.

Calculating your emergency fund

To calculate your emergency fund, work out your essential monthly expenses and multiply by the number of months you want to cover. This removes the guesswork and gives you a clear, achievable target. Reviewing your bank statements or budget planner can help you get an accurate picture of your monthly outgoings.

Simple emergency fund formula

Emergency fund target = essential monthly expenses × number of months

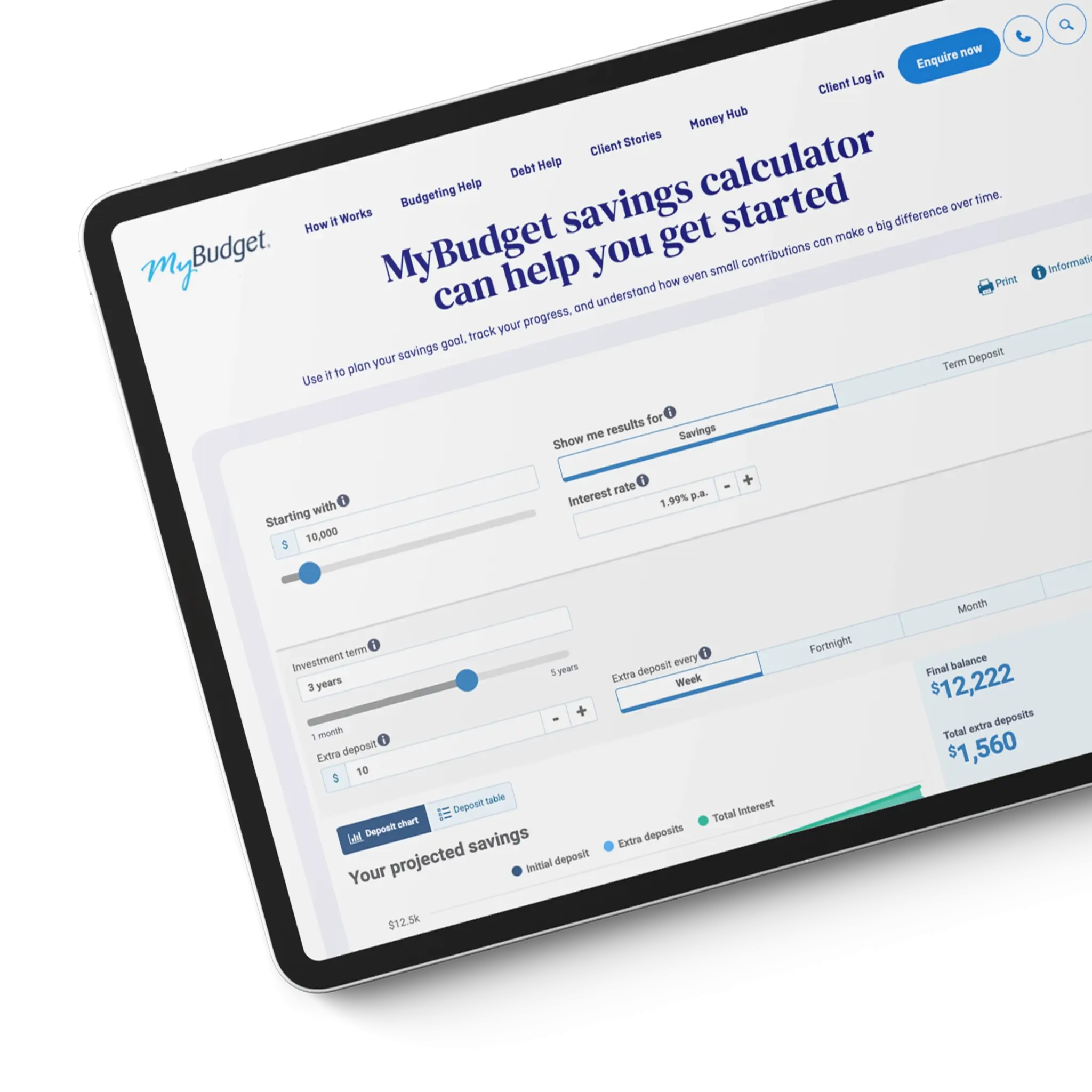

If you want a quicker way to work this out, you can use our free Savings Calculator (also useful as an emergency fund calculator) to estimate your target.

Example:

$3,500 × 3 = $10,500

This means your emergency fund target would be $10,500.

What to include when calculating your emergency fund

When calculating your emergency fund, focus on essential living expenses you would still need to cover if your income stopped. The table below outlines what to include.

Include | Examples |

Housing | Rent, mortgage |

Utilities | Electricity, gas, water |

Food | Groceries |

Transport | Fuel, public transport |

Insurance | Health, car, home |

Debt repayments | Minimum repayments |

Family essentials | Childcare, prescriptions |

How much emergency fund should you have based on your job type?

Your emergency fund target can vary depending on how stable your income is. If your income changes week to week, you may need a larger buffer than someone with a steady salary.

Casuals, contractors and gig workers

If your income is variable or unpredictable, an emergency fund is especially important. It gives you stability when your income does not always follow a set pattern. Without paid leave or guaranteed hours, any disruption can have an immediate financial impact.

For workers with fluctuating income, including casual roles, contract work, gig work and side hustles, aiming for three to six months of essential expenses can provide a stronger safety net over time.

Permanent workers

If you have a stable income and access to paid leave, your risk may be lower, but emergencies can still happen. Having savings in place means you are prepared, not caught off guard. Unexpected expenses or time off work can still create financial pressure.

For many permanent workers, one to three months of essential expenses can be a practical starting point, with the option to build further.

Emergency fund targets by work type

Your emergency fund target can vary depending on your job type and income stability. The table below shows a general guide based on how predictable your income is.

Work type | Why emergency money matters | Possible starting target |

Casual or gig work | Variable income, no paid leave | 3 to 6 months of essentials |

Contractor or self-employed | Income fluctuations, irregular work | 3 to 6 months of essentials |

Permanent full-time | More stability, but still exposed to risk | 1 to 3 months of essentials |

Permanent part-time | Some stability, lower income buffer | 1 to 3 months of essentials |

Where should you keep your emergency fund?

The best place to keep your emergency fund is in a separate, easily accessible savings account that is not linked to your everyday spending. This creates a clear boundary so your emergency money is there when you truly need it. An online savings account with a competitive interest rate can help your money grow while still being available when you need it.

This helps you:

- Access money quickly in a real emergency

- Avoid spending it on non-essential purchases

- Keep your savings organised and visible.

Look for an account with low fees, easy access, and conditions that suit how you save.

How to build an emergency fund: 5 simple steps

Building an emergency fund starts with small, consistent steps. You do not need to save large amounts straight away, you just need a plan you can stick to.

1. Create a budget

Start by understanding your income, expenses, and what you can realistically save. This gives you clarity and helps you feel more in control of your budget. Even small amounts build momentum. If you need help getting started, you can use our free Personal Budget Template to map out your income and expenses.

2. Set up automatic transfers

Automating your savings through automatic transfers or automatic deductions makes it consistent and removes the need to think about it each time, so you are building your emergency fund in the background.

3. Cut unnecessary expenses

Review subscriptions and spending habits to free up extra cash to redirect into savings. If you are not sure where to start, take a look at our guide to subscription creep to identify what you might be paying for without realising.

4. Use extra income wisely

If you earn additional income, consider putting part of it into your emergency fund instead of increasing spending, helping you reach your saving goals faster. Exploring side hustles can also be a practical way to boost your savings.

5. Avoid relying on credit like BNPL

Using credit cards or Buy Now Pay Later for everyday expenses can make it harder to build savings over time. If you want to understand the impact, read more about how BNPL can affect your finances.

How long does it take to build an emergency fund?

The time it takes to save an emergency fund depends on how much you can save and your target amount. The key is consistency and regularly reassessing your situation as your income or expenses change, so your plan continues to work for you.

Weekly savings | Time to reach $3,000 |

$25 | 120 weeks |

$50 | 60 weeks |

$75 | 40 weeks |

$100 | 30 weeks |

$150 | 20 weeks |

Ready to build your emergency fund with a plan that actually works?

If you have been meaning to start but are not sure where to begin, it can feel like there is never a right time. Getting ahead with money can feel overwhelming, especially when life keeps throwing things your way.

The good news is you do not have to figure it all out on your own, and you do not need to have it all perfectly mapped out to get started. With the right structure and support, building an emergency fund becomes clear, manageable, and achievable.

At MyBudget, we help you set up a personalised plan, stay on track, and build your emergency fund without sacrificing your lifestyle, so you can feel more in control of your personal finances.

Take the first step today and get in touch with MyBudget for a plan that works for your life.

or call us now on 1300 300 922.

Emergency fund FAQs

Can’t find what you’re looking for? See more FAQs…

Start small by setting aside what you can consistently, even if it is $10 or $20 a week. Focus on building your first $500 to $1,000 as a starting point, then grow it over time. Setting up automatic transfers and following a simple budget can help you build momentum quickly.

Most Australians should aim for around three months of essential living expenses as a starting point. This gives you a financial buffer if your income stops or an unexpected expense arises. If your income is less stable, building up to three to six months can provide extra security over time.

An emergency expense is something unexpected and necessary, such as medical bills, urgent car repairs, essential home repairs, or a sudden loss of income. It should not be used for everyday spending or non-essential purchases, even if they feel urgent at the time.

The best place to keep your emergency fund is in a separate, easily accessible savings account, such as an online savings account with a competitive interest rate. This allows your money to grow while still being available when you need it.

This article has been prepared for information purposes only, and does not constitute personal financial advice. The information has been prepared without taking into account your personal objectives, financial situation or needs. Before acting on any information in this article you should consider the appropriateness of the information having regard to your objectives, financial situation and needs.