Back

How to become debt-free in 2026: the financial reset you need

Get debt-free in 2026 with a clear, step-by-step guide to paying off debt, setting up a realistic budget and starting to live the life you want.

Ready for a financial fresh start

If becoming debt-free is on your 2026 goals list, you’re in the right place. January has a funny way of shining a spotlight on our finances. The credit card statements land, the interest charges sting a little more than usual, and suddenly the idea of a debt-free life feels both urgent and overwhelming.

Becoming debt-free in 2026 is achievable, even with interest rate uncertainty and the rising cost of living. It doesn’t require extreme sacrifices or giving up everything you love. What it does require is clarity, structure and a plan that works with your everyday life.

This guide is designed to help you reset, refocus and create genuine change. It walks you through how to get out of debt using practical budgeting, debt management strategies and the right tools and support, so you can work towards your financial goals with confidence.

What does becoming debt-free actually mean?

Becoming debt-free means clearing unsecured debt such as credit card debt, personal loans, car loans, BNPL services and other high-interest balances. For most people, it doesn’t mean paying off a mortgage immediately or avoiding all forms of credit forever.

Instead, it means removing the debts that cause the most financial stress and interest charges, so your income can be used to support your lifestyle, savings, financial goals and long-term wealth creation. For some people, this also includes credit repair and rebuilding confidence after a difficult period with debt. A debt-free life gives you breathing space, confidence in your finances and the freedom to focus on what comes next.

What’s the secret to get debt-free in 2026?

The difference between people who succeed and those who stay stuck in the debt cycle is not income, it is systems. Willpower can fade. Motivation comes and goes. But when your budget, debt repayments and savings are structured and automated, progress becomes visible and sustainable. That visibility is often the turning point.

Your debt-free checklist for 2026

If you want to start strong, begin with our checklist. This quick checklist helps you move from intention to action.

- Commit to becoming debt-free in 2026 and define what success looks like for you

- Gather all your financial information in one place before you start

- Decide whether your focus is speed, reducing interest, or lowering stress

- Choose a debt repayment method you can realistically maintain

- Set a clear intention for how debt freedom will change your lifestyle

- Give yourself permission to do this imperfectly, progress matters more than perfection.

Once these foundations are in place, real change becomes possible.

Step 1: Get crystal clear on your debt

Before choosing a debt repayment strategy, you need a full picture of your finances. This step is uncomfortable for many people, but it is also empowering.

Make a list of:

- Credit cards, balances and credit limits

- Credit card interest rates, interest fees and charges

- Personal loans, car finance and other unsecured debt

- BNPL services and short-term balances

- Minimum repayments versus total interest

- Your overall debt-to-income ratio.

Seeing everything in one place removes the guesswork and gives you options. Many people find it helpful to plug their numbers into a Debt Consolidation Calculator to understand how different repayment options could affect interest and timeframes.

Step 2: Choose a debt repayment strategy you can stick to

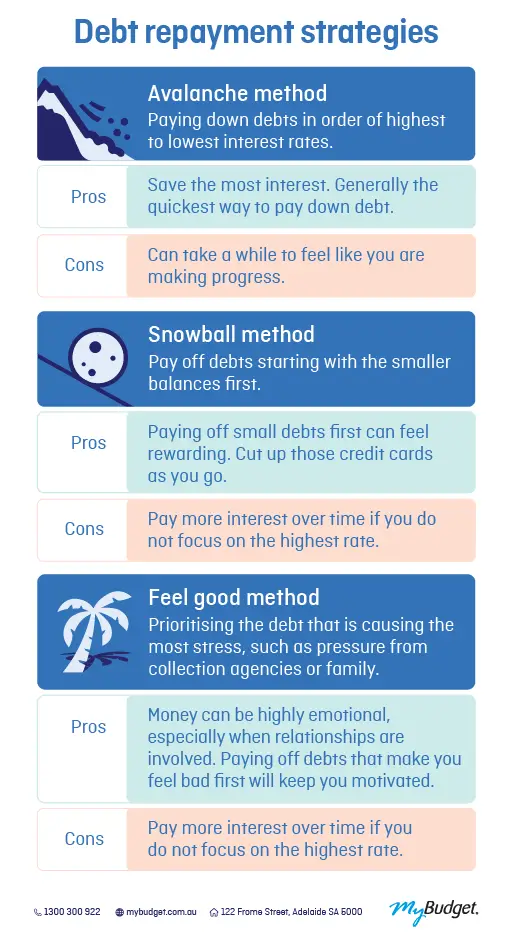

Not all debts are equal. Priority debts usually include high-interest credit card debt, BNPL services and access pay early loans with higher interest rates.

3 Common debt repayment strategies used in debt management plans are:

- Debt avalanche method: prioritising debts with the highest interest rate to reduce interest charges over time

- Debt snowball method: focusing on the smallest balances first to build momentum and confidence

- Feel good method: prioritising debts with the most stress, such as family pressure or debt collector.

Neither strategy is better on paper. The right one is the strategy you can follow consistently based on your mindset, financial stress levels and individual circumstances.

Step 3: Build a budget that supports debt reduction

A budget should not feel like punishment. It should feel like a plan.

A realistic budget:

- Covers essential expenses and lifestyle costs

- Allocates clear, achievable debt repayments

- Protects savings and an emergency fund

- Accounts for irregular and annual expenses

- Reduces reliance on credit cards.

When budgeting is automated and planned ahead, debt repayments stop competing with everyday spending. This is often where people finally break the cycle and start moving forward.

If you are thinking about starting a personal budget, it should support both your short-term debt repayments and your long-term financial goals. This type of budgeting help is a core part of effective debt management and long-term financial coaching. Having the right structure in place early can make the difference between short-lived motivation and lasting progress.

You can also download our free Personal Budget Template to help map out your income, expenses and debt repayments in one clear view.

Step 4: Put systems in place so debt stays gone

Paying off debt is a huge win, but staying debt-free requires a few smart systems.

Helpful guardrails include:

- Reducing credit card limits once balances are paid

- Being cautious with balance transfer credit cards

- Avoiding lifestyle creep as repayments reduce

- Using savings accounts for planned expenses

- Building an emergency fund for unexpected costs.

Without these protections, many people find themselves back in credit card debt within a year.

Step 5: Is debt consolidation the right option?

Debt consolidation can be helpful in the right circumstances, but it is not a magic fix. For some people, debt consolidation forms part of a broader debt solution or debt relief strategy, rather than a standalone answer.

A debt consolidation loan may be suitable if it:

- Lowers your overall interest rate

- Simplifies multiple repayments

- Fits comfortably within your budget.

However, debt consolidation without changes to spending habits often leads to more debt. If you are weighing up your options, check out our guide: debt consolidation: is it right for you? This can help you decide whether this approach suits your situation. This is why debt management programs that include budgeting, accountability and support are often more effective than relying on a loan alone.

How budgeting creates long-term financial freedom

Budgeting is not just about getting out of debt. It is what allows financial freedom to grow.

As debt repayments reduce, your budget can redirect money towards:

- Savings and emergency funds

- Long-term investing

- Wealth creation

- Retirement planning

- Homeownership and property goals.

This shift is where many people move from feeling stuck to feeling in control of their financial future. It is also where real stories matter. Megan and Creagh paid off $91,000 of debt with MyBudget, and their debt-free journey shows what is possible with the right structure and support.

What if your debt feels overwhelming right now?

If your debt feels unmanageable, it does not mean you have failed. Financial stress is incredibly common, especially during periods of economic pressure.

Sometimes the fastest way to get back on track is getting the right help. MyBudget offers a range of affordable debt relief solutions, including:

- Creditor negotiation to help reduce repayments or interest

- Credit card debt help to reduce high-interest balances

- Debt consolidation options to simplify multiple debts

- Credit score support through structured repayment management

- Debt agreements, such as Part 9 or Part 10 Agreements, for unmanageable debt

- Bankruptcy guidance when no other solution is suitable.

Get in touch with us for a plan to get out of debt, or explore our debt help options, so you can help you regain control, reduce stress and move forward with confidence.

Becoming debt-free starts with a budget

Becoming debt-free in 2026 is not about perfection or deprivation. It is about choosing progress, building systems that support your lifestyle and giving yourself the chance to move forward with confidence.

If you are ready to take the first step, starting a personal budget or getting in touch with us for a plan to get out of debt can help you create structure, reduce money stress and work towards a debt-free life. Living life free from money worries does not have to be a someday goal. You can start today.

Enquire online or call our expert Money Coaches on 1300 300 922.

Getting out of debt FAQs

Can’t find what you’re looking for? See more FAQs…

MyBudget is one of Australia’s most trusted budgeting and money-management services. For over 25 years, we’ve helped more than 130,000 Australians create personalised budgets, get out of debt, build savings, and reach their financial goals. We combine expert money coaching with powerful custom technology to organise your expenses, pay bills on time and take the stress out of managing money. MyBudget can help you build a plan that supports your long-term financial wellbeing.

The first step in comparing your lending options is completely free and without obligation. You can book a free home loan health check or initial call with a MyBudget Loans specialist to review your current mortgage and explore how much you could save through refinancing, which is a great way to start taking the weight off your shoulders.

When you join MyBudget, we ask your creditors to contact us on your behalf. Because of this, many clients experience fewer debt collector calls. We work with you to create a realistic repayment plan, organise overdue bills and show creditors your debts are being actively managed. While some contact may still occur, having MyBudget involved often provides reassurance and helps reduce stress and regain control.

Yes. MyBudget specialises in helping people with various levels of debt. We’ll work closely with you to create a customised plan aimed at reducing debt, managing expenses, and building savings, no matter your financial starting point.

It can have a positive impact if you make regular payments, but missed payments could hurt your credit.

Everyone’s financial situation and goals are different. That’s why our solutions are tailor-made for every client and our fees are based on the complexity and level of support you require with no lock-in contract.

This article has been prepared for information purposes only, and does not constitute personal financial advice. The information has been prepared without taking into account your personal objectives, financial situation or needs. Before acting on any information in this article you should consider the appropriateness of the information having regard to your objectives, financial situation and needs.