How financial hardship affects your credit score

11 min read

Struggling to manage overdue bills? Rising costs and interest rate hikes can feel overwhelming, but taking proactive steps to protect your credit score and creating a budget can help you regain financial control and avoid falling deeper into debt.

If you can’t pay your bills in Australia, the most important steps are to prioritise essential expenses, contact your creditors early to request financial hardship assistance, and create a realistic budget to prevent defaults.

Prefer to listen? Our hosts unpack this blog in a podcast episode, sharing practical steps for what to do when you can’t pay your bills, plus how MyBudget helps you reduce money stress and regain control of your finances.

Prefer to listen? Our hosts unpack this blog in a podcast episode, sharing practical steps for what to do when you can’t pay your bills, plus how MyBudget helps you reduce money stress and regain control of your finances.

When you can’t pay your bills, it’s easy to feel overwhelmed and bury your head in the sand. But ignoring overdue payments won’t make them disappear; it can lead to late fees, credit score damage, and mounting financial stress. The good news? Taking steps like contacting your service providers, setting up a payment plan, or getting help to protect your financial future is absolutely possible. Let’s walk through some practical strategies to help you reduce money worries and take back control of your finances.

It’s normal to feel overwhelmed but ignoring your bills will only add to the stress and late fees. Open your mail, log into your accounts and write down what you owe, who you owe it to and when payments are due. Getting a clear picture of the situation is the first real step to getting back in control.

When money is tight not all bills are created equal. Focus first on the basics such as your rent, mortgage, groceries, electricity, water and transport to work. These are your priority bills. Subscriptions, memberships and non-essential spending can be reduced or paused while you get your finances back on track.

The earlier you reach out the more options you usually have. Contact your lenders or service providers and ask about financial hardship programs, payment extensions or reduced repayment plans. You can also talk to a Budgeting Specialist who can help you put a plan in place. Acting early will prevent additional fees, defaults and unnecessary stress.

In February, the Reserve Bank of Australia (RBA) increased the cash rate to 3.85% and many Australian households are feeling the cost of living pressure. Mortgage repayments, personal loans, and credit card debt are still too high, leaving many households struggling to make ends meet.

On top of this, soaring energy bills, increasing food prices, and other everyday essentials have created a perfect storm of financial pressure for many households.

The aftermath of the pandemic is still being felt, with some people struggling to break poor money habits developed during lockdowns, while others are dealing with reduced savings and mounting debt after government support ended.

It’s a tough environment to manage, but with the right strategies such as budgeting, prioritising payments and seeking hardship assistance, there are ways to navigate financial difficulty and reduce stress.

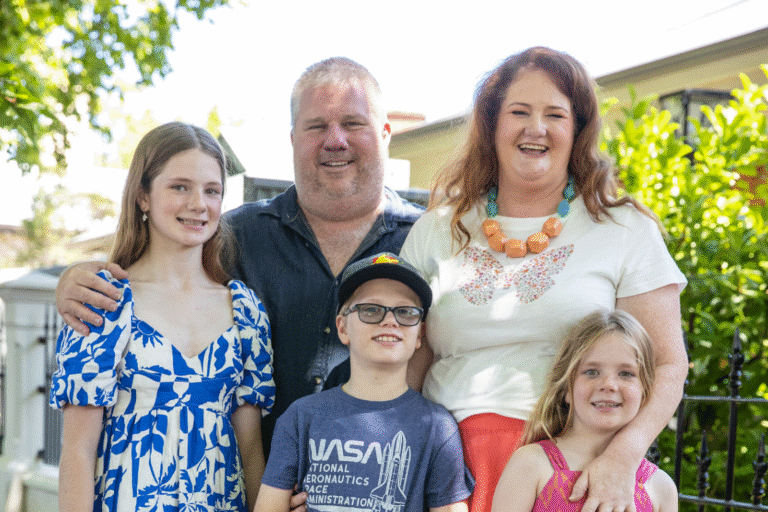

Alyssa and Pete’s journey shows how quickly debt and financial stress can spiral, even for households earning good incomes. After multiple miscarriages, they relocated for work and spent over $80,000 on IVF to build their family. With three children, rising daycare costs and more than $65,000 in debt, they were exhausted and stretched thin.

“I was so desperate to have these children, and then I never got to see them,” Alyssa stated. Despite working constantly, they felt like they were going backwards.

Their breaking point came with an $847 electricity bill Alyssa had missed. “I was sitting at my desk crying over this dumb bill,” she said. With no money left to cover it, she chose to call MyBudget and commit to a Personalised Budget Plan rather than take on another loan.

With structure, support and accountability, Alyssa and Pete paid off their debt, bought a home and eventually transitioned to living on a single income. Reflecting on the journey, Pete later admitted, “We never thought we’d actually get here.”

If you’re in a situation where your bills are out of control, don’t panic. Instead, take a deep breath and start working through these steps to regain control of your finances:

Your credit rating is your financial lifeline. A poor credit score can make it harder to get loans, secure rental properties, or access favourable interest rates in the future. If you’re struggling to pay your bills, focus on preventing defaults on your credit file.

Prioritise mortgage payments, rent, and utilities.Missing these payments can lead to serious consequences, including eviction or disconnection of essential services.

Don’t forget to contact other creditors early, including mobile providers, energy companies and credit card issuers. Ask about hardship or flexible repayment options before you miss payments, as they can report defaults to credit agencies.

If you want to find out more read our blog: How to clean your credit report and repair your credit score.

When money is tight, it can be tempting to rely on credit cards, Buy Now, Pay Later (BNPL) services, or access pay early loans to cover your expenses. But these options often increase your total debt and make it harder to recover.

Instead of adding new debt, focus on restructuring existing payments and reducing non-essential spending.

The worst thing you can do when you’re struggling to pay your bills is to do nothing. Financial problems don’t go away on their own; they escalate. Late fees, penalties, and reconnection costs can make a bad situation even worse.

Open your bills, list what you owe and contact providers to request payment extensions or hardship arrangements. Many companies in Australia are required to have financial hardship policies in place.

A personal budget is your most powerful tool for regaining control of your finances. Start by listing your income and expenses to get a clear picture of your financial situation. If you’re not sure where to begin, download our free Personal Budget Template to make the process easier.

Look for areas where you can cut back. Small savings can add up over time. For example, consider reducing your streaming subscriptions, cutting back on takeaway meals, or shopping around for better utility rates.

If your income fluctuates, focus on covering your essential expenses first, like housing, food, and utilities. A budget will also help you negotiate with creditors by showing them what you can realistically afford to pay.

When your bills are more than your income, you need to prioritise payments. Start by asking yourself:

For example, it’s more important to keep your electricity on than to pay for a streaming service. Similarly, ensuring your insurance remains active is more critical than keeping up with a gym membership.

Also, look for ways to reduce your household expenses. Compare energy providers, phone plans, and insurance policies to find better deals.

If you know you won’t be able to make a payment on time, contact your creditors and service providers as soon as possible. Ask about reduced payments, payment holidays or temporary extensions under their hardship policy.

Be honest about your situation and provide any relevant documentation, such as a personal budget. The earlier you act, the more likely you are to avoid debt collection, default listings, bankruptcy or legal action.

If you’re feeling overwhelmed, financial counsellors offer free, confidential and independent guidance to help you understand your options, navigate financial difficulty, and feel more informed about the decisions in front of you.

If you’re looking for a personalised service tailored to your unique financial situation, ongoing support can make all the difference. At MyBudget, we work alongside you to create a realistic budget, manage your bills, negotiate with creditors where needed, and build a plan that supports your goals. Your dedicated Money Coach is there to guide you every step of the way, helping you stay on track and move forward with confidence.

Financial stress can feel overwhelming, but you don’t have to go through it alone. At MyBudget, we’ve helped over 130,000 Australians take control of their finances and achieve financial freedom.

We’ll work with you to create a budget that fits your situation, negotiate with creditors and build a practical plan forward. There’s no obligation to get started, and your first chat with one of our friendly Money Coaches is completely free.

Let us help you live your life free from money worries. Enquire online or call 1300 300 922 today.

Can’t find what you’re looking for? See more FAQs…

If you miss payments, you may be charged late fees and your creditor can issue default notices. Utility providers may disconnect services and lenders can report missed payments to credit reporting agencies. Contacting providers early and requesting financial hardship assistance can prevent escalation.

Prioritise essential living expenses: rent or mortgage, electricity, water, food and transport to work. These keep your household functioning. Non-essential subscriptions and memberships can usually be paused.

In Australia, energy providers must follow hardship and disconnection guidelines. They cannot disconnect you without notice and must offer payment plans. Contact them early if you’re struggling.

This article has been prepared for information purposes only, and does not constitute personal financial advice. The information has been prepared without taking into account your personal objectives, financial situation or needs. Before acting on any information in this article you should consider the appropriateness of the information having regard to your objectives, financial situation and needs.